Best Banks in UAE: A Complete Guide to the Country’s Leading Financial Institutions

The Best banks in UAE continue to strengthen their position through strong assets, digital banking innovation, customer-focused services, and resilient financial performance. From FAB and Emirates NBD to ADCB, Dubai Islamic Bank, Mashreq, and HSBC UAE, the country’s banking sector remains one of the most trusted and competitive in the Middle East, serving residents, businesses, investors, and global clients.

Best banks in UAE

The Best banks in UAE in 2026 are not simply the biggest balance sheets; they are the lenders that convert scale into earnings, digital convenience, service quality and regulatory credibility. By that yardstick, FAB leads on sheer size and credit strength, Emirates NBD on retail scale and digital execution, ADCB on sustained earnings momentum and service modernization, DIB on Islamic banking depth, and Mashreq on digital-first and cross-border capability. That conclusion is supported by official disclosures, CBUAE data and corroborating coverage from UAE outlets including The National, Gulf News and Khaleej Times.

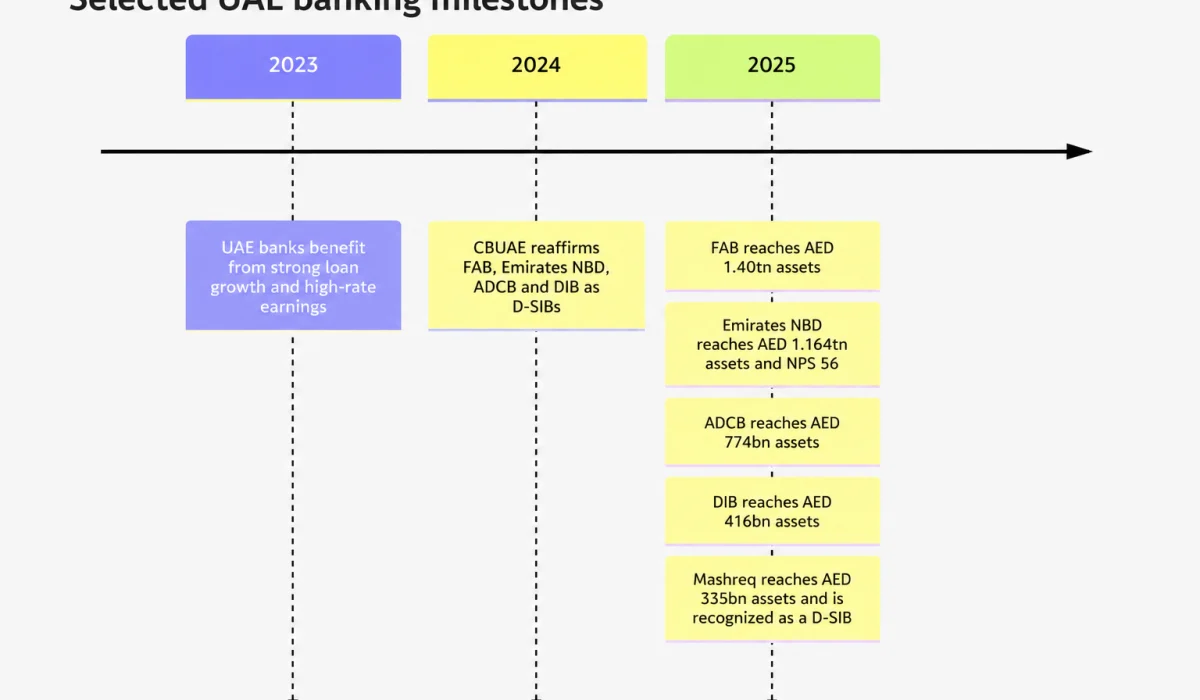

At year-end 2025, FAB reported AED 1.40 trillion in total assets and AED 21.11 billion in net profit, keeping its position as the UAE’s largest lender. Emirates NBD reported AED 1.164 trillion in assets and AED 24.0 billion in net profit; ADCB reached AED 774 billion in assets and AED 11.445 billion in net profit after tax; DIB reached AED 416 billion in assets with AED 9.0 billion in pre-tax profit; and Mashreq posted AED 335 billion in assets and AED 8.3 billion in pre-tax profit. Against CBUAE’s AED 5.3399 trillion banking-system asset base at end-2025, those five banks represented roughly 76.6% of system assets combined, by straightforward calculation from reported figures.

Recent results show that the leaders are still extending the gap. In the first quarter of 2026, FAB’s total assets rose to AED 1.490 trillion and quarterly net profit reached AED 5.034 billion. ADCB reported AED 809 billion in assets and a record AED 3.781 billion in profit before tax. DIB reported AED 420 billion in assets and AED 2.1 billion in pre-tax profit. Emirates NBD said its assets stood at AED 1.2 trillion as of 31 March 2026, serving more than 10 million active customers.

A useful cross-check comes from regional rankings. In Forbes Middle East’s 30 Most Valuable Banks 2025, FAB ranked third in the region, Emirates NBD sixth, ADCB eighth, DIB thirteenth and Mashreq seventeenth. In the broader Top 100 Listed Companies 2025, Emirates NBD ranked sixth, FAB seventh, ADCB tenth, DIB twenty-second and Mashreq twenty-third. That means the UAE banking leaders are not just domestically dominant; they remain among the Middle East’s most valuable listed financial institutions.

The timeline below summarizes selected milestones that shaped the current ranking.

How the leaders compare

FAB is the best choice for investors and large corporates who prioritize scale, sovereign-linked strength and international breadth. Fitch reaffirmed FAB’s AA- rating in May 2026 and highlighted its strong domestic franchise, liquidity and systemic importance. FAB also has a presence in 20 markets, giving it a wider cross-border platform than most domestic peers.

Emirates NBD is arguably the strongest all-rounder for retail and affluent banking. Its 2025 annual report disclosed 9.8+ million active customers, 787 branches across 13 countries, NPS of 56, and record profitability. The group also said it commands a 35% market share of UAE credit card spend, a notable franchise indicator in consumer banking.

ADCB stands out as the fastest-improving universal bank. It delivered 19 consecutive quarters of profit-before-tax growth by Q1 2026, has 47 branches in the UAE, 560+ ATMs, and was recognized as the highest-ranked bank in the UAE in KPMG’s UAE Customer Experience Excellence Report, while Brand Finance rated it the country’s strongest banking brand in 2025.

DIB remains the leading pure Islamic banking name in the UAE. Its investor-relations fact sheet describes it as the largest Islamic bank in the UAE, serving more than 11 million customers through 540+ branches and 900 ATMs groupwide. Its 2025 results also showed improving asset quality, with the non-performing financing ratio falling to 2.65%, then to 2.5% in Q1 2026.

Mashreq is smaller than the top four by assets, but it keeps punching above its weight. It reported the lowest NPL ratio in the sector at 1.0% for 2025, a 20% ROE, and continued investment in AI, digital onboarding and cross-border services. For customers prioritizing international corridors, digital journeys and corporate connectivity, it remains one of the most credible alternatives to the larger incumbents.

Digital banking and customer experience

Digital execution is now a primary separator among the best UAE banks. Emirates NBD said its mobile platforms serve more than 2.5 million active users, supported by 50+ AI initiatives and the region’s first AI-powered contact-centre platform. FAB said in February 2026 that it had more than 30 agentic AI use cases progressing across trade, payments, compliance and operations, and later launched a fully digital Payit Universal Account aligned with CBUAE’s financial-inclusion framework. ADCB launched a next-generation AI-powered mobile app in May 2026. DIB said its alt app offers 135+ services, handled 51% of customer transactions in 2025, and that 80% of new-to-bank customers were onboarded digitally. Mashreq’s 2025 results pointed to deeper AI deployment across onboarding, lending, credit decisioning and fraud prevention.

Because the UAE does not have one mandatory, standardized public customer-service league table across all banks, the cleanest comparable indicators are a mix of disclosed service metrics and public digital ratings. Emirates NBD’s reported NPS of 56 is one of the strongest bank-published service indicators visible in this research. ADCB’s KPMG recognition is a useful independent service marker. As a public digital proxy, Google Play snapshots showed ratings of roughly 4.7 for ENBD X, 4.7 for Mashreq, 4.4 for FAB Mobile, 4.1 for ADCB, and 3.6 for DIB alt; these figures are directional rather than audited and can change.

Three remarks from market leaders and regulators capture the tone of the market well:

“continues to demonstrate the highest levels of resilience and stability.” — H.E. Khaled Mohamed Balama, Governor, CBUAE.

“The Bank delivered a strong performance … marking 19 consecutive quarters of profit growth.” — Ala’a Eraiqat, Group Chief Executive Officer, ADCB.

“The quarter reflects healthy business momentum … and the continued strength of the Bank’s core franchise.” — Dr. Adnan Chilwan, Group CEO, DIB.

Regulation and outlook

The regulatory context matters because in the UAE, “best” banking franchises are inseparable from prudential strength. CBUAE’s 2024 annual report said the UAE banking sector reached a record AED 4.56 trillion in assets in 2024 and reaffirmed FAB, Emirates NBD, ADCB and DIB as domestic systemically important banks, each subject to higher capital buffers. By March 2026, the central bank said sector assets had climbed above AED 5.42 trillion, with a sector capital adequacy ratio of 17% and LCR above 146.6%. In February 2026, CBUAE also issued a guidance note on the responsible use of AI, underscoring that digital innovation now sits squarely inside the supervisory perimeter.

That framework is one reason the ranking above favors institutions that combine strong balance sheets with digital modernization. FAB and Emirates NBD remain the closest thing to UAE banking blue chips; ADCB has become the sector’s most compelling challenger among large universal banks; DIB is the standout Islamic franchise; and Mashreq remains a high-quality specialist with unusually strong asset quality and digital momentum.

Methodology and limitations

This assessment prioritizes primary sources: CBUAE publications, annual reports, audited interim statements, investor-relations fact sheets and bank press releases. UAE-based outlets such as Gulf News, The National and Khaleej Times were used mainly to corroborate interpretation and recent context. Unless otherwise noted, balance-sheet data are FY2025 year-end figures, with Q1 2026 updates added where official releases were available. Market-share figures in this article are derived calculations using bank-reported 2025 assets against CBUAE’s reported Q4 2025 banking-system assets. A key limitation is that customer-service ratings and branch-network disclosure are not standardized across UAE banks; where exact cross-bank comparables were unavailable, the article used published NPS, independent customer-experience recognition, public app-store ratings and official branch/ATM pages as proxies.

Comments

No comments yet — be the first to start the conversation.